How Credit Default Swaps Influenced the 2008–2009 Financial Crisis?

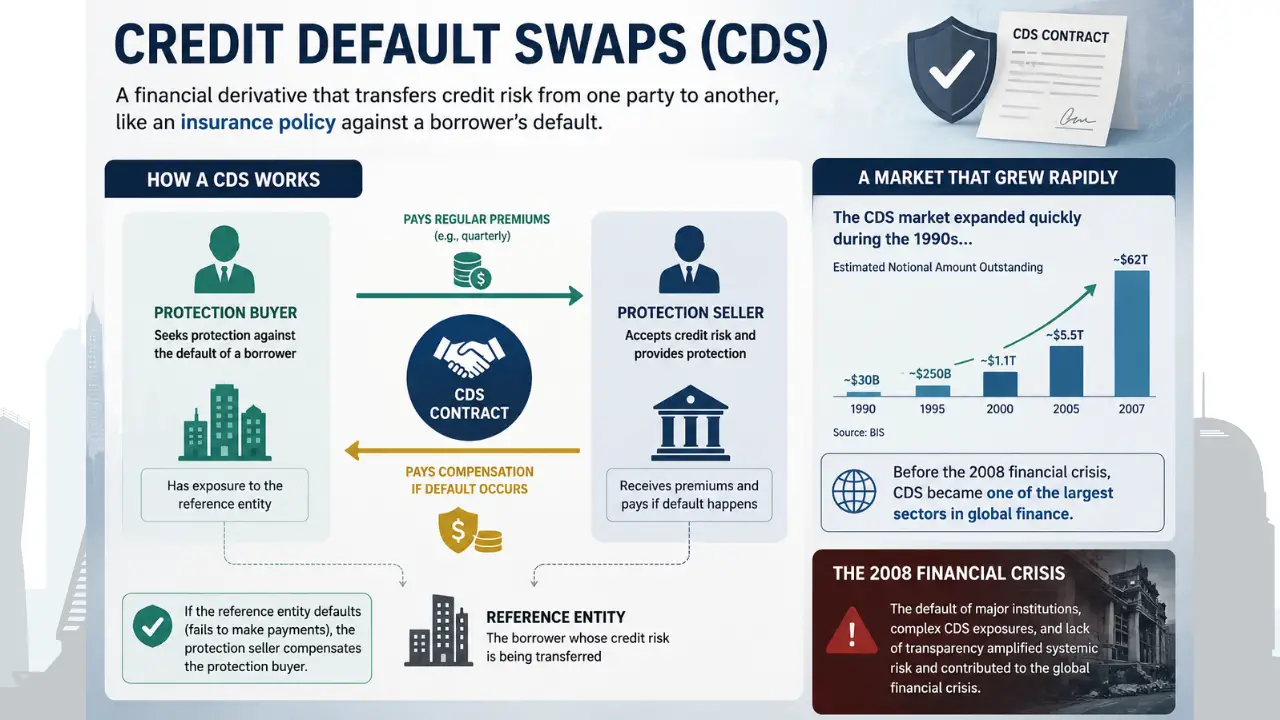

Credit Default Swaps (CDS) are financial derivatives used to transfer credit risk from one party to another. They operate similarly to insurance contracts, where the buyer pays regular premiums in exchange for protection against a borrower’s default. The CDS market expanded rapidly during the 1990s and became one of the largest sectors in global finance before the 2008 financial crisis.

CDS were widely used because they allowed banks and investors to hedge risk, improve lending capacity, and measure default probabilities more efficiently. However, during the 2008–2009 financial crisis and the European sovereign debt crisis, CDS also revealed major weaknesses related to liquidity, transparency, and market incentives. As a result, CDS became viewed as both risk management tools and potential amplifiers of financial instability.

Theoretical Benefits of CDS

One of the main benefits of CDS is risk transfer. Banks can reduce their exposure to risky loans without selling assets, allowing them to free up capital and increase lending activity. CDS also improve price discovery because CDS spreads often react faster to changes in credit conditions than bond yields, making them a more sensitive indicator of default risk.

Additionally, CDS improve market efficiency by allowing investors to hedge and manage credit exposure more effectively. Before CDS existed, investors had limited ways to protect themselves against credit losses without selling bonds or loans.

Practical Shortcomings of CDS

Practical Shortcomings of CDS

Despite their advantages, CDS markets showed major weaknesses during financial crises. One of the biggest problems was market opacity, as regulators and institutions lacked visibility over the total amount of CDS exposure in the system. This became clear during the collapse of Lehman Brothers, where institutions struggled to identify counterparty risks.

Another issue was illiquidity. Sovereign CDS markets were often shallow, meaning even small trades caused large movements in spreads and increased market volatility. CDS also created the “empty creditor problem,” where investors protected by CDS could benefit more from default than debt restructuring, reducing incentives for cooperation during financial distress.

Furthermore, naked CDS positions allowed investors to speculate on defaults without owning the underlying bonds, increasing pressure on sovereign debt markets and amplifying contagion during the European debt crisis.

CDS During the 2008–2009 Crisis

CDS did not directly cause the financial crisis, but they amplified existing weaknesses in the financial system. Synthetic CDOs used CDS contracts to increase exposure to mortgage-backed securities, which magnified losses when mortgage defaults rose.

The collapse of American International Group (AIG) highlighted these risks. AIG sold large amounts of CDS protection without holding enough collateral, leading to severe losses during the crisis. Sovereign CDS also increased market fear during the European debt crisis, particularly in countries such as Greece, Portugal, Italy, and Spain.

However, some economists argue that CDS mainly exposed deeper structural problems such as poor fiscal management, weak governance, and excessive lending rather than creating the crisis themselves.

Reforms After the Crisis

After the crisis, regulators introduced reforms to improve transparency and reduce systemic risk in CDS markets. The European Union restricted naked sovereign CDS positions, while the International Swaps and Derivatives Association standardized CDS settlement procedures through the Big Bang Protocol. Basel III regulations also increased capital and liquidity requirements for banks to strengthen financial stability.

Conclusion

Overall, CDS provided important benefits such as risk transfer, improved price discovery, and greater market efficiency. However, the 2008–2009 financial crisis showed that CDS could also amplify financial instability through opacity, illiquidity, contagion, and speculative trading. Therefore, CDS were not the direct cause of the crisis but acted as amplifiers of existing weaknesses within the global financial system.

By Amir Amidian

Senior Market Analyst | Zylostar

A CDS is a financial derivative that provides protection against the risk of a borrower defaulting on their debt, similar to an insurance contract.

Because they allowed banks and investors to hedge credit risk, improve lending capacity, and estimate default probability more efficiently.

In stable markets, yes—they help transfer and diversify risk. However, during crises, they can also amplify systemic risk due to liquidity and transparency issues.

CDS did not cause the crisis, but they amplified losses through excessive risk exposure, lack of transparency, and institutions like AIG failing to cover their obligations.

It occurs when investors holding CDS protection prefer a borrower to default rather than restructure debt, because they benefit more from the payout.

U.S. stock futures moved higher early Thursday as investors assessed a fresh round of Big Tech ea...

U.S. stock futures traded higher early Friday as Wall Street looked to build on a strong rebound,...

China's semiconductor industry celebrated a major milestone as ChangXin Memory Technologies (...

U.S. stocks ended mixed on Tuesday as strong corporate earnings, lower oil prices, and a shift aw...

U.S. stock futures traded mixed early Friday as investors awaited the closely watched July employment report, a key i...

SpaceX has reached a pivotal milestone as its lock-up period expires, allowing millions of previously restricted shar...

Star investor Cathie Wood has strengthened her bullish stance on artificial intelligence by purchasing $17.6 million ...