Zylostar Market Wrap – April 3, 2026

U.S. labour market data surprised to the upside, with Nonfarm Payrolls printing at 178K, significantly above the 65K forecast, while private payrolls surged to 186K. The unemployment rate edged down to 4.3%, reinforcing resilience in the labour market. However, wage growth softened to 3.5% YoY, suggesting some easing in inflationary pressures. Meanwhile, labour force participation ticked slightly lower to 61.9%, and government payrolls remained weak.

Following the data, traders scaled back expectations for Federal Reserve rate cuts in 2026, as the stronger employment picture supports a more cautious policy stance.

On the geopolitical front, tensions in the Middle East remain elevated. Escalation between Iran and regional actors continues to disrupt key infrastructure and energy routes, with fresh attacks reported across Gulf states, including damage to energy facilities in Kuwait and operational disruptions in Abu Dhabi. The Strait of Hormuz remains a focal point, with limited signs of reopening despite ongoing negotiations. Former President Donald Trump added to the volatility, suggesting the U.S. could take control of the strategic waterway if given more time.

Oil markets reacted sharply, with crude prices holding above $110 per barrel, supported by supply concerns and continued threats to regional stability.

Equity markets showed mixed performance. Asian stocks edged higher into the close, supported by optimism around potential trade flow improvements, while U.S. equity futures drifted lower, with S&P 500 contracts down modestly. European and several global markets remained closed for Easter holidays, contributing to subdued liquidity and limited price action across asset classes.

In fixed income, Treasury futures traded largely unchanged during the Asian session, with cash markets closed in major financial centres. The U.S. dollar traded mixed against G10 peers as investors positioned ahead of further macro developments.

Looking ahead, markets will remain highly sensitive to geopolitical headlines over the weekend, particularly any developments around the Strait of Hormuz and Middle East conflict dynamics. Additionally, evolving expectations around Federal Reserve policy will continue to drive cross-asset volatility in the sessions ahead.

By Amir Amidian

Senior Market Analyst | Zylostar

Because data > headlines (for now). Strong NFP and private payrolls shifted focus back to U.S. economic resilience, delaying panic-driven risk-off moves.

Rate cut expectations got hit. The market is now pricing fewer cuts in 2026 as the labour market proves it’s still too strong for the Fed to ease aggressively.

It’s not demand — it’s supply risk. The Hormuz situation is the key. As long as that remains unstable, oil has a strong floor.

Mixed regime.

Macro → risk-on (strong data)

Geopolitics → risk-off

That’s why you’re seeing choppy price action instead of clean trends.

Easter holidays = thin markets.

That means:

Moves can be slower

But spikes can be aggressive if news hits

Allies of U.S. President Donald Trump are stepping up efforts to reshape the Federal Reserve, fue...

The U.S. labor market delivered mixed signals, with nonfarm payrolls rising by just 57,000 jobs i...

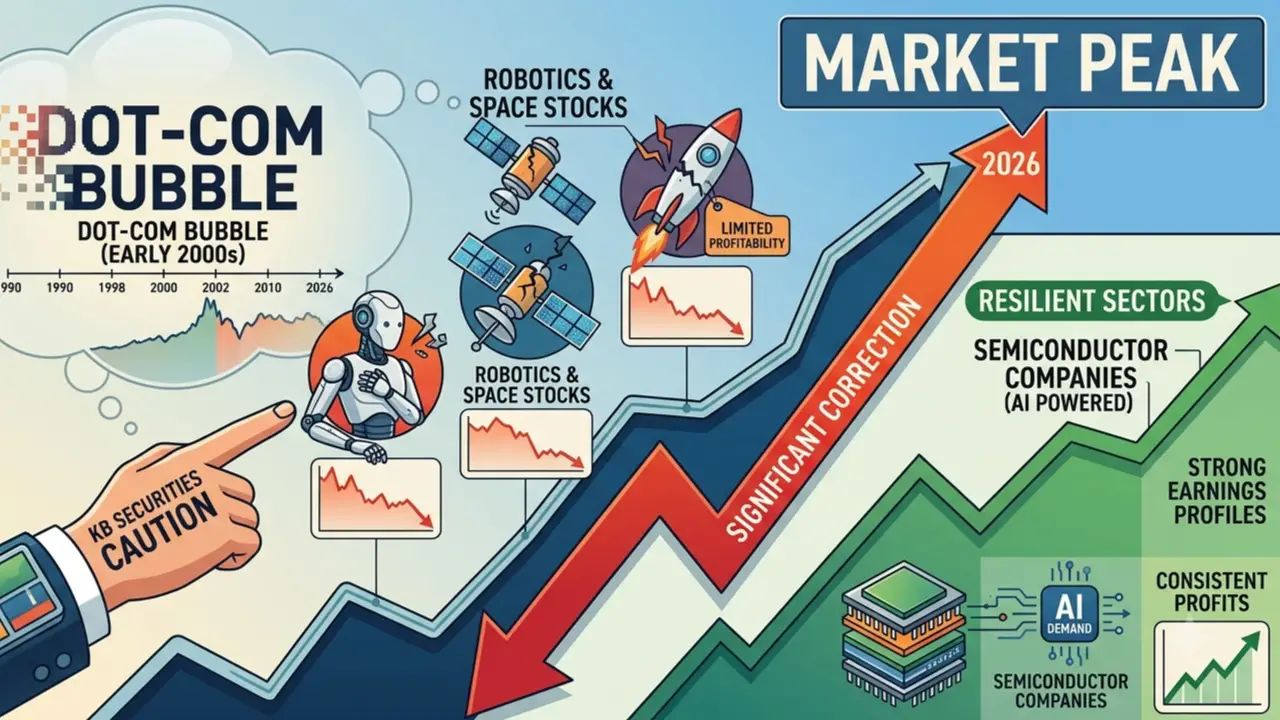

KB Securities has cautioned that robotics and space-related stocks may be among the most exposed ...

SpaceX shares fell for a third consecutive session, erasing nearly $600 billion in market value a...

Welcome back to another Zylostar Market Update. In this week's technical market analysis, we break down the la...

The global economy delivered mixed signals this week as U.S. job growth continued to slow while Eurozone inflation ea...

Global stock markets closed higher on Friday, led by strong gains across Europe and Asia, while U.S. markets remained...